Articles

Effective Investment Strategies

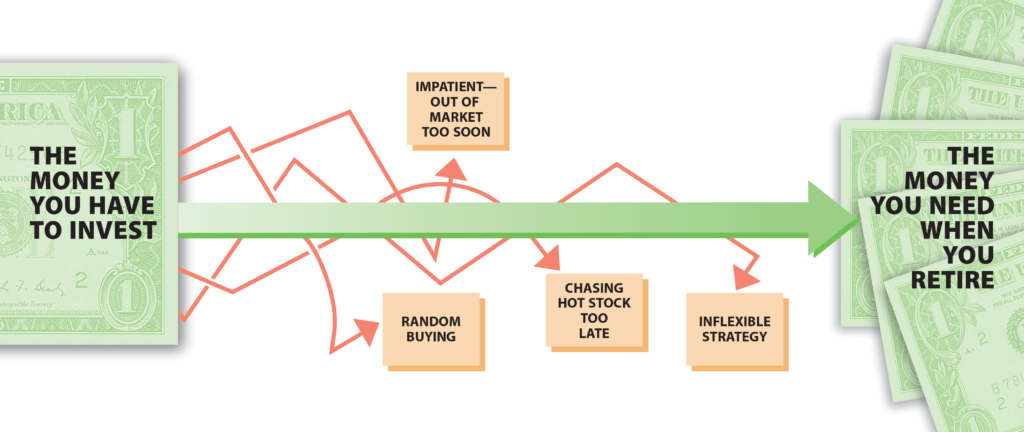

A great strategy doesn’t guarantee a win, but investing without a game plan compounds the risk of coming up short….

A great strategy doesn’t guarantee a win, but investing without a game plan compounds the risk of coming up short.

Random buying and selling—adding a few stocks here, redeeming a bond there—is rarely an effective strategy for planning retirement income. To be a successful investor, you have to follow two seemingly contradictory pieces of advice: Stick with your investment strategy but stay flexible. That means having a long-term perspective but not getting locked into choices that don’t work as you expected.

By knowing how different investments can affect your portfolio, the level of income you want to produce, and how much risk you are willing to take, you’ll have a stronger opportunity—though, of course, not a guarantee—of ending up where you want to be financially.

STRATEGIC DECISIONS

The amount you can withdraw from your retirement accounts depends on the size of your account, the return it provides from year to year, and the number of years you need income. Losses early in the withdrawal period seriously limit long-term return.

MOVING IN NEW DIRECTIONS

If your emphasis has been on building an equity portfolio, you may want to consider starting to invest in income-producing investments, including intermediate and long-term bonds and bond funds.

Among the factors to consider are the bonds’ ratings—unless they are US Treasurys—their terms, and the interest rates they pay. A question with longer-term issues is whether you’re willing to commit your principal at the current market rate if rates seem likely to increase in the future.

While they’re not right for all investors, limited partnerships, real estate investment trusts (REITs), or equipment leasing programs may be possible income producers.

DRAWING ON PRINCIPAL

While preserving principal is critical while you’re investing for retirement, there’s nothing wrong with planning to use some of the principal—say 4% to 5% a year—after you retire. But, you need a plan for tapping your resources, similar to a withdrawal schedule for your IRA, and a sense of which investments to liquidate.

A maturing CD, for example, can become a source of current income. When it comes due, you can deposit the principal in a money market or savings account to draw on as you need cash. That might be smarter than withdrawing money from an investment that’s doing well, like a stock fund, or selling real estate when prices are low.

APPROACHES TO PLANNING

There’s no way to protect yourself completely from market volatility without taking on inflation risk. But there may be ways to produce a stream of income while maintaining some long-term growth. One approach is to deposit dividends or distributions from certain equity investments into a spending account. That’s a departure from the strategy of reinvesting all earnings to buy additional shares, which is appropriate as you build your retirement savings. But this regular source of income can supplement your living expenses or pay for extras.

At a certain point—which is different for different people—you may also begin selling certain stocks or stock mutual funds that have increased in value and reinvesting the money in income-producing investments. If you ladder, or stagger, the maturity dates of the bonds and CDs you purchase, you can either redeem them when they come due and add the principal to your spending account or buy a replacement.

Remember, though, that there are no guarantees in investing. While the markets could be strong in any period, you could also have flat or falling returns and even lose principal.

ANTICIPATING INCOME FOR THE LONG TERM

The amount you can withdraw from your retirement accounts depends on the size of your account, the return it provides from year to year, and the number of years you need income. Losses early in the withdrawal period seriously limit long-term return.